TKT RESEARCH DESK · MAY 2026 · 10 MIN READ

Real Assets. Digital Yields. The TKT tagline is compact. Behind it is a more complicated idea — and one that most investors, even sophisticated ones, haven’t fully worked out yet.

In short

This is about a new category of financial product that sits between real estate and crypto — and why the gap between those two worlds is where some of the most interesting yield opportunities of the next decade are forming. TKT is the first structured product built specifically for that gap.

The Problem That Built This Product

Here is a situation most serious real estate investors know well. You commit capital to a deal. The project is solid. The numbers are good. And then you wait — eighteen months, sometimes three years — before you see meaningful return. The asset is performing. Your capital is just locked up while it does.

That illiquidity is not a flaw in real estate. It is the price of stability. Real estate works because it is hard to move — the same quality that protects it from the volatility of liquid markets also traps the capital inside it.

On the other side of the same problem: crypto markets offer liquidity, 24/7 settlement, and the kind of upside that traditional assets rarely touch. What they lack is floor. Most crypto yield products cannot tell you, plainly and verifiably, where the return comes from. Ask hard enough and you find token inflation, leveraged positions with no backstop, or incentive structures that depend on continuous inflows to sustain themselves.

Investors are stuck choosing between trust and performance. That is the gap TKT was built to occupy.

Token House Token was created by a team with backgrounds on both sides of this — traditional finance structuring and crypto engineering — to build something that does not force that choice.

Why This Is Happening Now

For most of the past decade, the idea of bringing real-world assets on-chain was theoretical. The technology existed. The legal frameworks did not. The investor appetite was speculative, not structural.

That has changed considerably in the past two years.

The on-chain tokenised real-world asset market grew 380% in three years — from roughly $5 billion in 2022 to over $30 billion by the end of 2025. Real estate is the largest single category within that growth.

Source: RedStone, Gauntlet & RWA.xyz, Real-World Assets in On-chain Finance Report, 2025.

Source: RedStone, Gauntlet & RWA.xyz, Real-World Assets in On-chain Finance Report, 2025.

The regulatory picture is also clarifying. The UAE’s VARA issued an explicit framework for RWA tokenisation in 2025. Singapore’s MAS expanded its digital asset licensing. The EU’s DLT Pilot Regime, launched in 2023, is now being made permanent with broader scope.

None of this happened because regulators suddenly became enthusiastic about crypto. It happened because the asset class reached a scale where ignoring it was more expensive than engaging with it.

The forecasts for where this goes vary. BCG and ADDX project $16 trillion in tokenised assets by 2030 — roughly 10% of global GDP. McKinsey is more conservative, estimating $4 trillion. The direction is the same in every model: up, and fast.

BCG & ADDX, ‘Relevance of On-chain Asset Tokenization in Crypto Winter’ (2022); McKinsey & Company, ‘From Ripples to Waves’ (2024).

Why Do Most RWA Products Fail to Deliver Real Yield?

Here is the part that does not get discussed enough in the market commentary: most tokenised real estate products have solved the wrong problem.

Fractionating a property is technically interesting. Putting ownership on-chain adds transparency. Reducing the minimum investment from $500,000 to $5,000 is genuinely democratising. But none of these solve the core investor problem: how do you generate yield from the asset without waiting for a sale or refinancing event?

A 2025 academic paper — “Tokenize Everything, But Can You Sell It?” (arXiv:2508.11651) — documented what this looks like in practice. The authors found that tokenised real estate tokens showed minimal secondary market activity and almost no active trading — the thesis was proven, but the market wasn’t built.

The third failure is opacity. Most tokenised real estate projects do not publish on-chain records of property acquisition, rental income, or expense ratios. Investors are asked to trust a black box with a blockchain label.

The real breakthrough in tokenised real estate is not making a property cheaper to access. It is building an architecture that generates yield from the asset while the asset itself appreciates — and doing it with enough transparency that an investor can verify the numbers themselves.

What TKT Actually Is

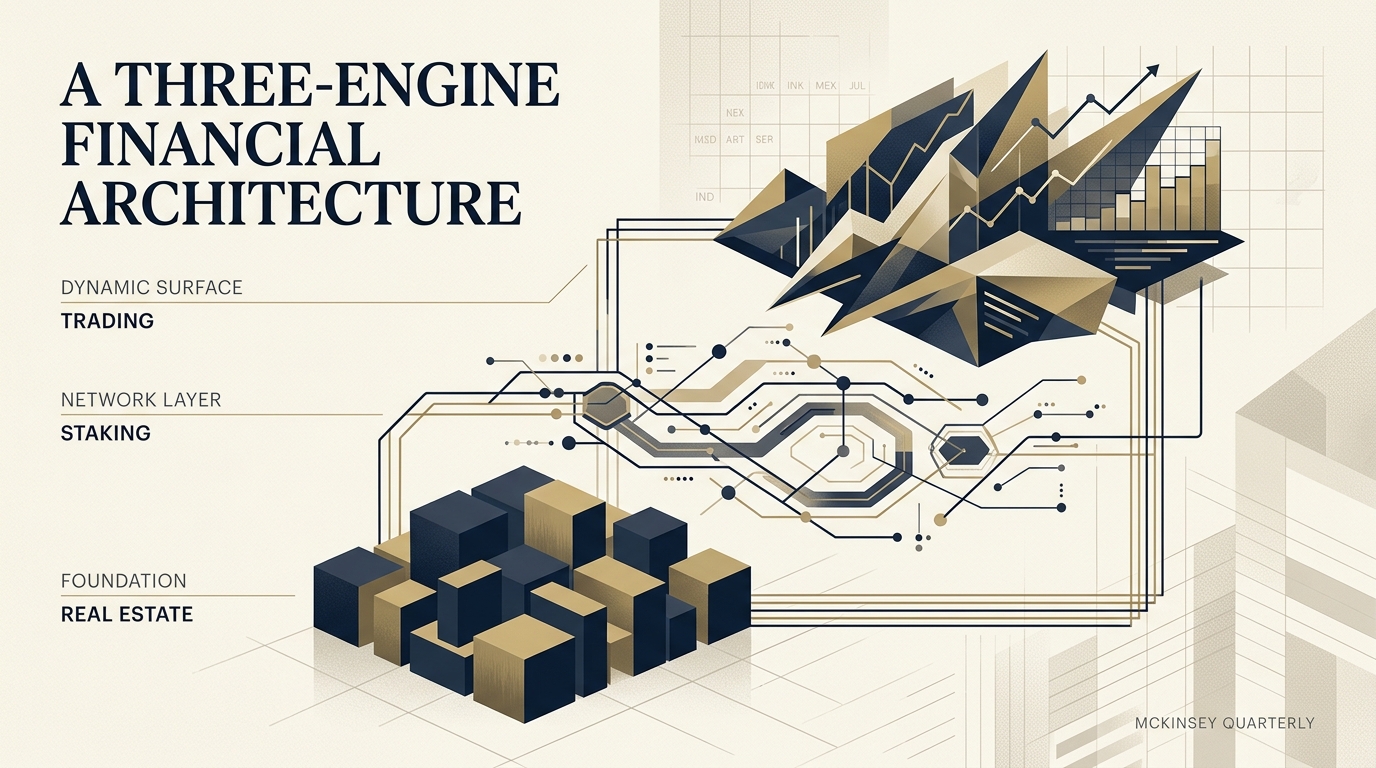

TKT describes itself as the first structured product that combines real estate, trading, and staking in a single on-chain token. That description is accurate, but it understates how unusual the architecture is.

Start with the asset foundation. Each TKT node is a dedicated LLC that holds U.S. real estate — specifically Section 8 affordable housing. These are not speculative developments. They are income-generating rental properties with government-backed payment streams. The yield from rental income is distributed monthly.

On top of that real estate foundation, 20% of each node’s capital goes into stablecoin staking protocols — generating additional yield from the liquid portion of the balance sheet. This is not leverage in the traditional sense. The staking capital is separate from the property capital. A problem in one does not cascade into the other.

The third engine is proprietary trading — and this is where the architecture becomes genuinely unusual. The trading does not use investor capital. It uses a separate trading allocation, with profits shared into the node. Each node must bank three months of advance trading profits before full distributions begin — meaning the buffer is capital already earned and held in reserve, not a tolerance for losses.

The three engines are independent. A problem in one — a slow month for trading, a delayed property sale — does not cascade into the others. This is the structural difference between TKT and most tokenised real estate products: it is designed for resilience, not just for access.

Phase 1 of TKT is the LLC-based structure described above. Phase 2 — currently in roadmap — moves toward direct title-deed tokenisation, where each property is represented by on-chain tokens with full legal ownership transfer capability.

The Investor This Is Built For

TKT is not a retail product. The minimum node participation is $250,000 USDT. It is built for investors who already have real estate exposure and are looking for a more liquid, higher-yield format — or for crypto-native investors who want real-world backing without giving up the performance they are used to.

The profile that fits best: a portfolio in the $500,000–$2M range allocating 10–20% to alternative assets. Comfortable holding for 12–24 months. Values transparency over marketing. Has already been burned by a DeFi protocol that promised yields it could not explain.

The profile that does not fit: anyone looking for immediate liquidity, anyone who needs guaranteed returns, anyone not comfortable reading an on-chain transaction record.

The transparency argument is worth dwelling on, because it is TKT’s answer to what is legitimately the hardest objection in this space: how do I know the asset is real? Every property acquisition, rental payment, and expense ratio is published on-chain. The LLC operating agreements are available for review. The trading records are verifiable. This is not marketing transparency — it is structural transparency, built into the architecture.

The Bigger Picture

Real estate tokenisation is, right now, at roughly the same stage as internet banking in 1999. The infrastructure works. The regulatory frameworks are forming. The early adopters are already using it. The mainstream still thinks it is a fringe idea.

What is already clear is what the mature version of this market looks like: real-world assets that are programmable, liquid, and transparent — without giving up the stability that makes them worth holding in the first place.

TKT’s roadmap extends that logic forward. Energy grids. Data centres. Satellite infrastructure. The same three-engine architecture — real asset foundation, staking layer, trading overlay — can be applied to any income-generating physical asset.

The question for investors evaluating this space in 2026 is not whether real-world asset tokenisation becomes significant. It already is. The question is which products are built to survive the transition from early adoption to mainstream use — and which are built to capture the hype.

The first structured product in a new asset class does not need to be perfect. It needs to be honest, verifiable, and architecturally sound. That is the standard TKT was built for.

Explore the TKT architecture → tkt-vault.co

Full whitepaper → tokenhousetoken.com

FAQ

Q: What is Token House Token (TKT)?

A: TKT is a structured financial product that combines three income engines in a single on-chain token: U.S. real estate (Section 8 affordable housing), stablecoin staking, and proprietary trading. Each node is a dedicated LLC with on-chain transparency.

Q: What is real-world asset (RWA) tokenisation?

A: The process of converting ownership rights in a physical or financial asset — real estate, a bond, a commodity — into digital tokens on a blockchain. This allows fractional ownership, transparent record-keeping, and programmable transfer of value.

Q: Why Section 8 housing specifically?

A: Section 8 — the U.S. Housing Choice Voucher Programme — pays rent directly from housing authority budgets to landlords. This creates a government-backed income stream with lower default risk than market-rate rentals.

Q: Is TKT regulated?

A: TKT operates as an unregulated product in Phase 1. The team has chosen on-chain transparency — every transaction verifiable, every property record public — as the primary investor protection mechanism. Phase 2 includes regulatory licensing in multiple jurisdictions.

Q: How does the trading engine work without risking investor capital?

A: TKT’s LLC balance sheets are disclosed to trading platforms as proof of solvency, which unlocks access to higher-value trading strategies. The trading allocation is separate from investor capital. Profits are shared into the node; losses are absorbed by the trading buffer.

Q: What happens to the market for tokenised real estate by 2030?

A: BCG and ADDX project $16 trillion in tokenised assets by 2030 — with real estate forecast to become the largest single category. McKinsey estimates $4 trillion. Either way, the direction is clear: real-world assets on-chain will be a significant part of global finance.