TKT Research Team · MAY 2026 · 9 MIN READ

The 90/90/90 Rule — Why Crypto Returns Fail and How TKT Was Built to Survive It

In short

90% of new traders lose 90% of their capital in the first 90 days. The same pattern plays out across most crypto yield products when markets shift. The failure is not bad luck — it is bad architecture. This post covers the three ways yield products break, what a sound product needs to avoid each one, and how TKT was built with exactly these problems in mind.

Why Do Most Crypto Yield Products Fail?

Every crypto cycle produces a new generation of yield products. Every cycle ends the same way: the returns look exceptional on the way up, the structure gets tested on the way down, and most products don’t survive. The post-mortem always blames market conditions. That is not wrong — but the real issue is that these products were never built to handle bad conditions. They were built for good ones.

Three failure modes come up repeatedly. Each has a specific fix.

What Is the First Way Yield Products Break?

The most common yield mechanism in DeFi pays depositors in the protocol’s own newly minted token. You receive tokens — that part is real. But the tokens are being inflated to pay you. While new money keeps entering and demand outpaces supply growth, the numbers hold up. When inflows slow, inflation wins, the token price falls, and the yield in dollar terms collapses — usually faster than the headline APY ever suggested.

The token’s value is circular: it depends on the inflow of capital that the yield is designed to attract. When the loop breaks, the yield disappears with it.

The fix: yield paid in USDT or USDC, generated from an activity that does not need a constant stream of new investors to keep functioning.

What Is the Second Failure — and Why Is It Structural?

High-yield crypto products frequently use leverage to amplify returns. It works well in calm or rising markets. In a sharp move down, leveraged positions get liquidated — fast and fully. The yield was real. The floor was not. This is the mechanism behind the 90/90/90 rule — backed by retail broker disclosure data required by UK and EU financial regulators: roughly 90% of retail participants in leveraged trading lose roughly 90% of their capital within the first 90 days. Not because they made poor decisions. Because the structure exposes them to losses with nothing underneath.

The fix: trading that runs on completely separate accounts from investor capital. If the trading goes wrong, it stays on the trading side — not in the investor’s wallet.

What Is the Third Failure Most Investors Don't Know About?

Many yield products distribute returns as they come in — or worse, distribute in advance and rely on future performance to cover the gap. When a losing stretch hits, there is nothing to absorb it. Distributions stop. Or the protocol mints more tokens to cover what it promised, which loops straight back to Failure 1.

The fix: a mandatory buffer that has to be built before distributions can exceed the baseline. Bank three months of trading profits first, and a losing month can be absorbed without interrupting payments or touching principal.

The products that survive bad markets are not lucky. They are built differently from the start.

How Is TKT Built Differently?

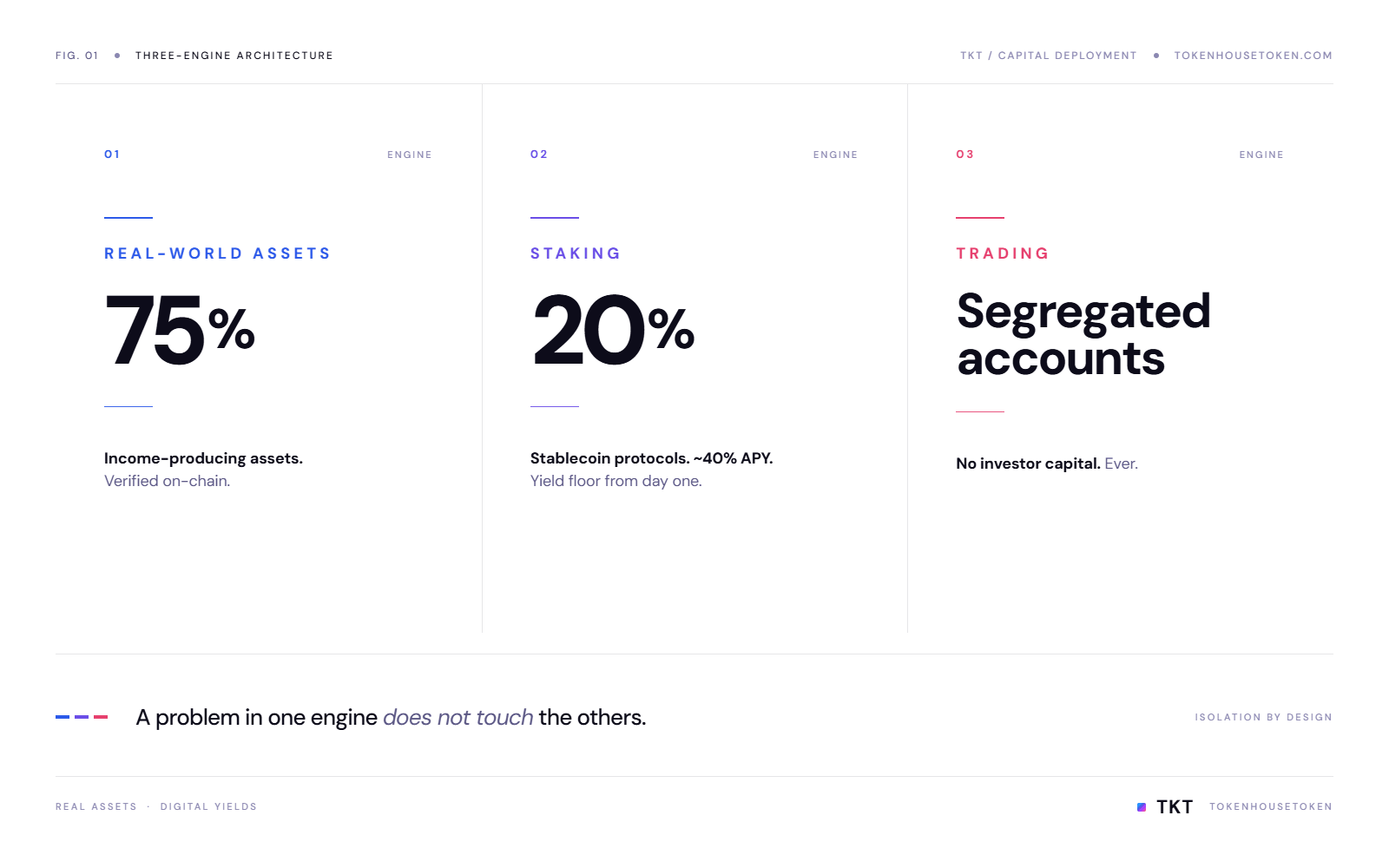

TKT’s yield system treats each of the three failures above as a design constraint. Three independent income engines, each addressing a different risk.

Real-world assets — 75% of node capital

Three-quarters of every USDT deposited into a TKT node goes into income-producing real-world assets. The income does not depend on crypto markets, token prices, or new investor inflows. It comes from physical assets generating real economic yield. Every acquisition is documented — verified records available to TKT holders on request.

Stablecoin staking — 20% of node capital

Twenty percent goes into stablecoin staking protocols generating approximately 40% APY. The maths: $1 invested → $0.20 staked → 40% APY → $0.08 per year → roughly 0.67% per month per $1 deployed. Modest, but it matters. It starts on day one, before the real asset engine has had time to mature, and it provides the floor that protects distributions in slow trading months.

The protocols used are established, audited, and carry no currency exposure. The capital is also liquid, which supports redemptions.

Proprietary trading — segregated accounts

This engine generates performance above the staking floor. The critical point: it does not use investor capital. TKT’s LLC balance sheets are disclosed to trading platforms as proof of solvency, which unlocks access to higher-value proprietary trading accounts. The trading happens on completely separate accounts. No investor USDT is in them.

The traders have a 2.5-year record generating over 60% annually across gold (XAUUSD), equity futures, and crypto. Monthly performance is distributed in USDT, capped at 2.5%–5% per month. Anything above 5% in a given month stays in the reserve — building the buffer rather than being distributed immediately.

How Does the Performance Buffer Actually Work?

Before full distributions begin, each TKT node must accumulate three months of advance trading profits. This is not a contractual promise — it is capital that has already been earned and set aside. It absorbs losing months without touching distributions or principal.

A worked example: a 1,000,000 TKT node must hold $150,000 USDT in reserve ($0.05 per token × 3 months) before full distributions start. If a trading month produces nothing, the buffer covers the gap. Holders receive the staking floor. The buffer rebuilds in the months that follow. Principal stays untouched.

A permanent 7.5% capital reserve runs alongside this — not a yield number, but structural insulation against exceptional drawdown.

TKT is built around the floor: real asset income that is independent of crypto markets, a stablecoin staking baseline, a three-month buffer that absorbs bad months, and a 7.5% reserve behind that. The trading engine adds performance on top. But the foundation comes first.

What Happens in a Losing Trading Month?

- Trading distribution for that month: zero

- Staking yield (~0.67% per month per $1 deployed) is credited to holder wallets

- The three-month buffer absorbs the shortfall

- Principal is unaffected — it is not in trading accounts

- The buffer rebuilds before full distributions resume

None of this is a guarantee. Real-world asset values can fall. Staking protocols can have technical issues. Trading can underperform for extended periods. But because each risk layer is separate — real assets, staking, trading — a problem in one does not automatically hit the others. That is the answer to the 90/90/90 problem.

FAQ

Q: What is the 90/90/90 rule in trading?

A: The 90/90/90 rule is a widely cited observation — supported by regulatory disclosure data from brokers in the UK, EU, and Australia — that roughly 90% of retail traders lose roughly 90% of their capital within the first 90 days of trading. It reflects how leveraged trading is structured, not the skill level of the people involved.

Q: Does TKT use investor capital for trading?

A: No. TKT's trading engine runs on proprietary accounts funded by platform credit, unlocked by disclosing TKT's LLC balance sheets as proof of solvency. Investor USDT never enters trading accounts.

Q: What is TKT's minimum monthly yield target?

A: 2.5% per month, backed by the staking baseline and the three-month performance buffer. The maximum cap on distributions is 5% per month. Anything above 5% in a given month stays in the reserve.

Q: How does the three-month performance buffer work?

A: Each node must bank three months of advance trading profits before full distributions begin. That capital has already been earned — it is sitting in reserve to absorb bad months without stopping payments or touching principal. The protection is mathematical, not contractual.

Q: What happens in a losing trading month?

A: Trading distribution for that month is zero. Staking yield is credited to holder wallets. The three-month buffer absorbs the shortfall. Principal is unaffected — it is not in trading accounts. The buffer rebuilds in subsequent months before full distributions resume.

Q: What happens to real estate appreciation in TKT?

A: Real estate appreciation is retained by the platform — it is not passed to token holders. The redemption value is capped at $1 per TKT, the original contribution. Investors earn through monthly yield distributions. This keeps the redemption process straightforward.

Explore the TKT architecture → tkt-vault.co

Full whitepaper → tokenhousetoken.com

Ready to understand how TKT generates yield?

Explore the architecture and start earning structured yield on real assets.